BNG Market Update: June 2025 Pricing Report Shows Growing Stability

For property developers navigating Biodiversity Net Gain, understanding market pricing and trends isn't just helpful - it's essential to make informed purchasing decisions.

That's why we're pleased to share our latest BNG Pricing Report for June 2025, drawing on data from 77 habitat banks across England.

This comprehensive analysis - our largest dataset yet - provides the market intelligence you need to secure the right units at the right price. This supports our mission to deliver clients BNG Certainty and our promise of "the best price BNG with guaranteed results”.

This blog is a summary of the report’s key findings.

To get the full June 2025 BNG Pricing & Insights Report in your inbox: click here

Market Stability Emerges

After 17 months since mandatory BNG implementation, we're seeing signs of the market maturing. Unit prices have shown only minor fluctuations this quarter. This stability provides developers with greater confidence when budgeting for BNG requirements and planning project timelines.

However, some habitat banks are beginning to offer strategic discounts on out-of-area units to help offset the impact of Spatial Risk Multipliers, creating new opportunities for cost-conscious developers willing to source units from adjoining or national catchments.

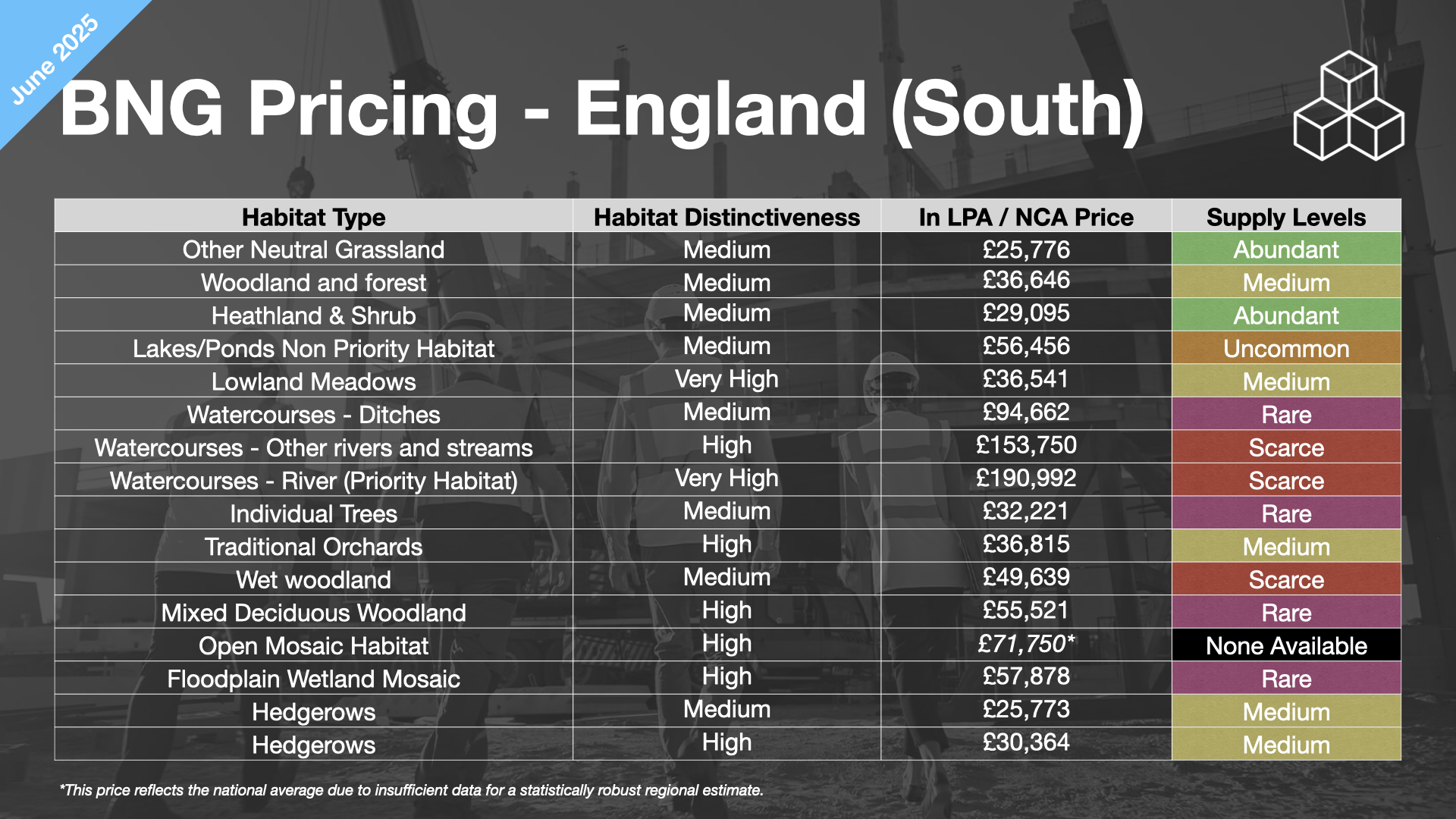

Watercourse Units: The Supply Challenge Continues

One of the most significant findings in our June report concerns watercourse units, which remain in short supply across England. Demand for watercourse units continues to rise, yet supply remains extremely limited.

As a result, many developers are being forced to purchase units from out-of-area suppliers, often incurring a 2x Spatial Risk Multiplier. For developers with projects affecting ditches, rivers, or streams, this supply shortage presents both a challenge and a planning imperative.

Early engagement with BNG suppliers becomes even more crucial when watercourse units are required, as limited availability often means developers must accept higher costs or extended timelines.

A More Diverse Supply Market Takes Shape

The BNG supply landscape is evolving into a healthier, more balanced ecosystem. Whilst established multi-site operators like Environment Bank, Green Earth Group, and Nattergal continue to play important roles, we're seeing significant growth from independent firms and smaller landowners entering the market.

This diversification benefits developers by increasing choice and competition. Since February 2025, the number of habitat banks on the Natural England Register has more than doubled - rising from 43 to 90 registered sites. This significant growth expands both market capacity and geographic coverage across England.

Not only does this demonstrate the market's continued growth, it offers opportunities to landowners of all sizes.

Geographic Imbalances Reveal Opportunities

Our analysis reveals interesting patterns in supply distribution across England. Some National Character Areas (NCAs) are becoming well-served by habitat banks, whilst others face significant supply constraints.

Areas such as the Shropshire, Cheshire and Staffordshire Plain, Southern Pennines, and The Fens now host multiple habitat banks. Conversely, urban areas including the Manchester Conurbation, Inner London, and South Coast Plain remain significantly underserved.

For developers, these geographic patterns highlight the importance of early planning and flexible sourcing strategies, particularly when working in supply-constrained areas.

New Unit Types Expand Options

The June report includes several newly tracked habitat types, reflecting improved supplier availability and market sophistication. We've added three distinct watercourse categories, Open Mosaic Habitat, and additional hedgerow classifications to our pricing analysis.

This expansion in available unit types provides developers with more precise matching options for their specific project requirements, potentially reducing costs through better habitat alignment.

Looking Ahead…

The data shows a market that's finding its rhythm. With more registered habitat banks, greater supplier diversity, and increasing standardisation of processes, the BNG market is clearly progressing from early adoption into a more stable operational phase.

For developers, this maturing market translates to greater certainty in planning, more competitive pricing, and improved confidence in project delivery timelines.

Ian Hambleton, Founder & Director of Biodiversity Units UK, commented:

"The June 2025 report shows a market coming of age. With 77 habitat banks now in our analysis and genuine price stability emerging, developers can approach BNG with much greater confidence than even six months ago. However, the acute shortage of watercourse units remains a significant challenge that requires careful planning and early action. We're committed to helping developers navigate these complexities and secure the best possible outcomes for their projects."

Get BNG Certainty with us

Whether you're planning your first BNG purchase or managing multiple developments, understanding these market dynamics is crucial for success. Our quarterly reports provide the market intelligence you need to make informed decisions and avoid costly mistakes.

As always, we welcome feedback on how to make this report even more useful. We’ll continue to publish quarterly updates.

Stay informed! Sign up for future BNG Pricing Reports

To get the full June 2025 BNG Pricing & Insights Report in your inbox: click here